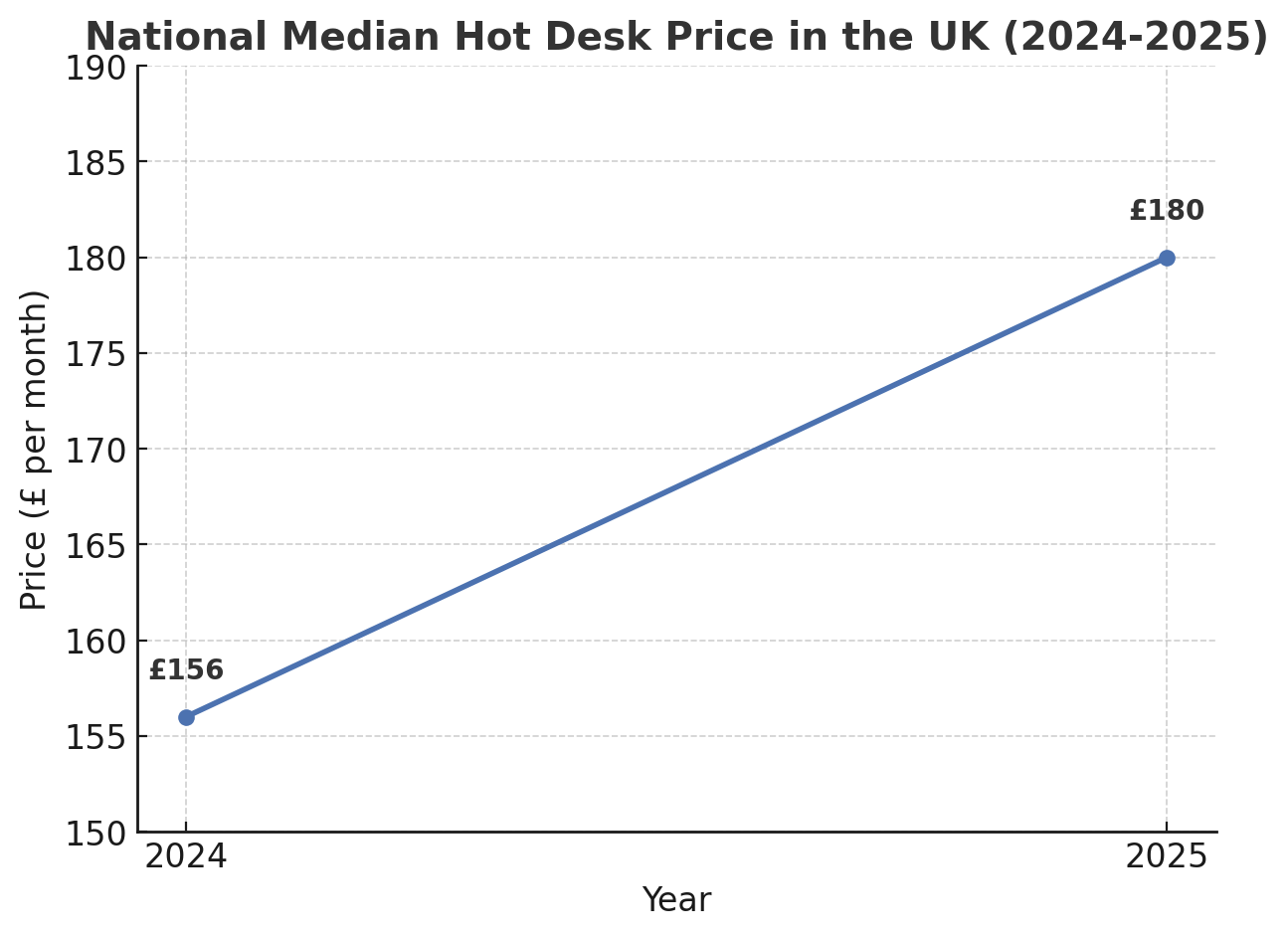

Rural and small-town coworking prices

In rural and suburban areas, prices can be dramatically lower. Hot desks under £100/month are common, often offered by small operators or cooperatives catering to local freelancers, remote workers, and microbusinesses.

While these spaces may operate on smaller budgets, they often trade on community appeal and hyper-local networking.

Key takeaways for UK based coworking space operators

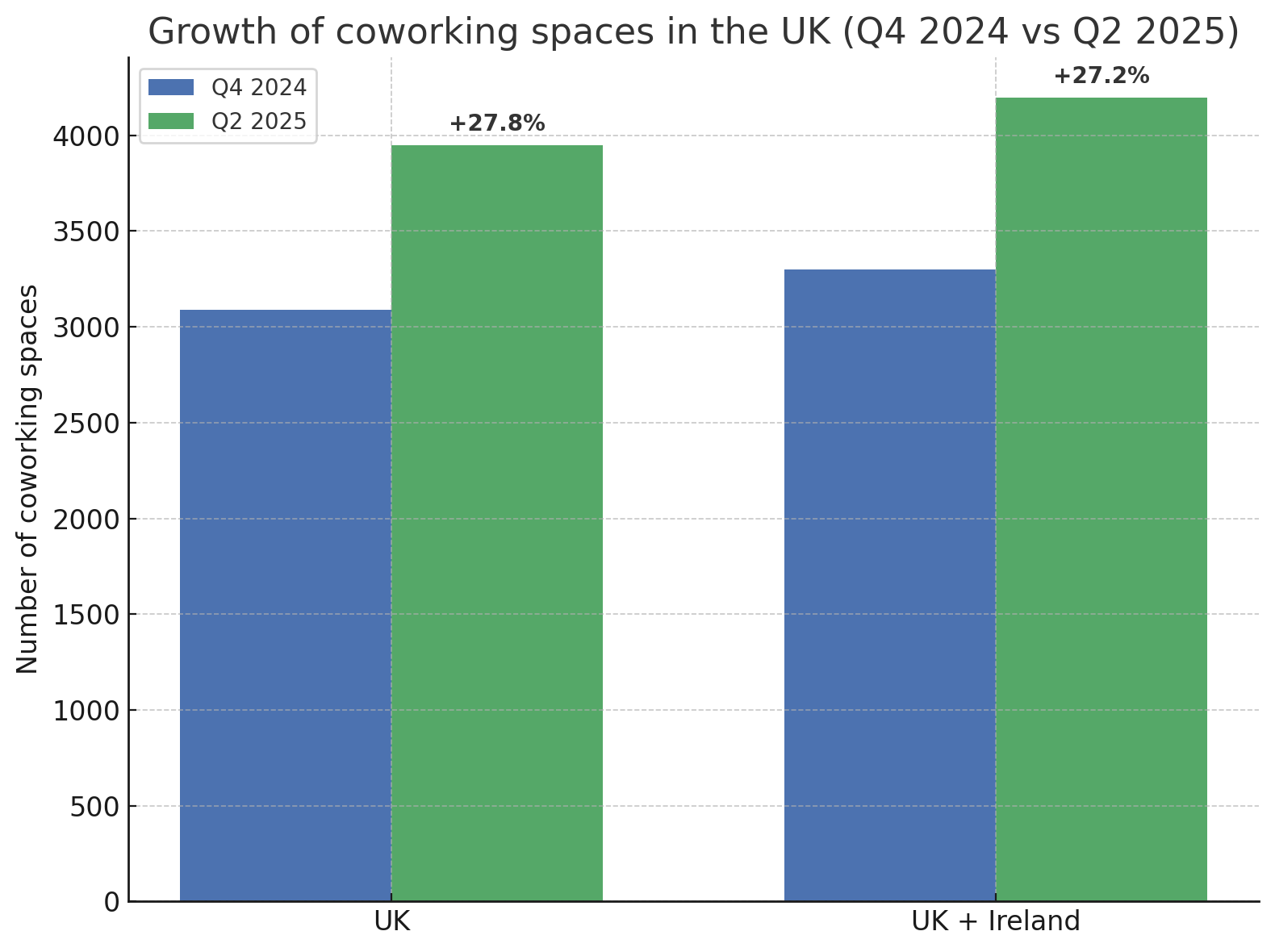

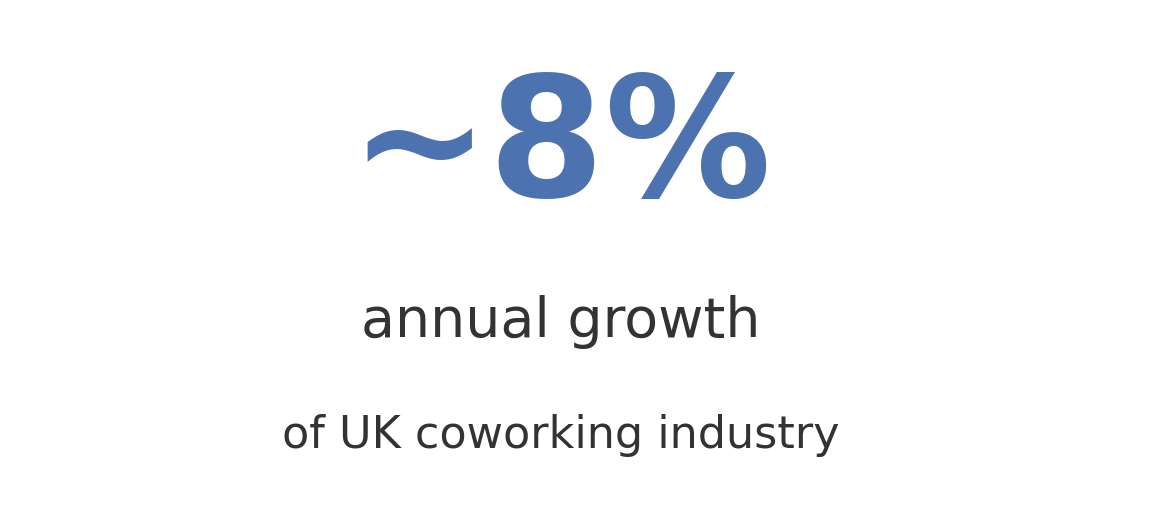

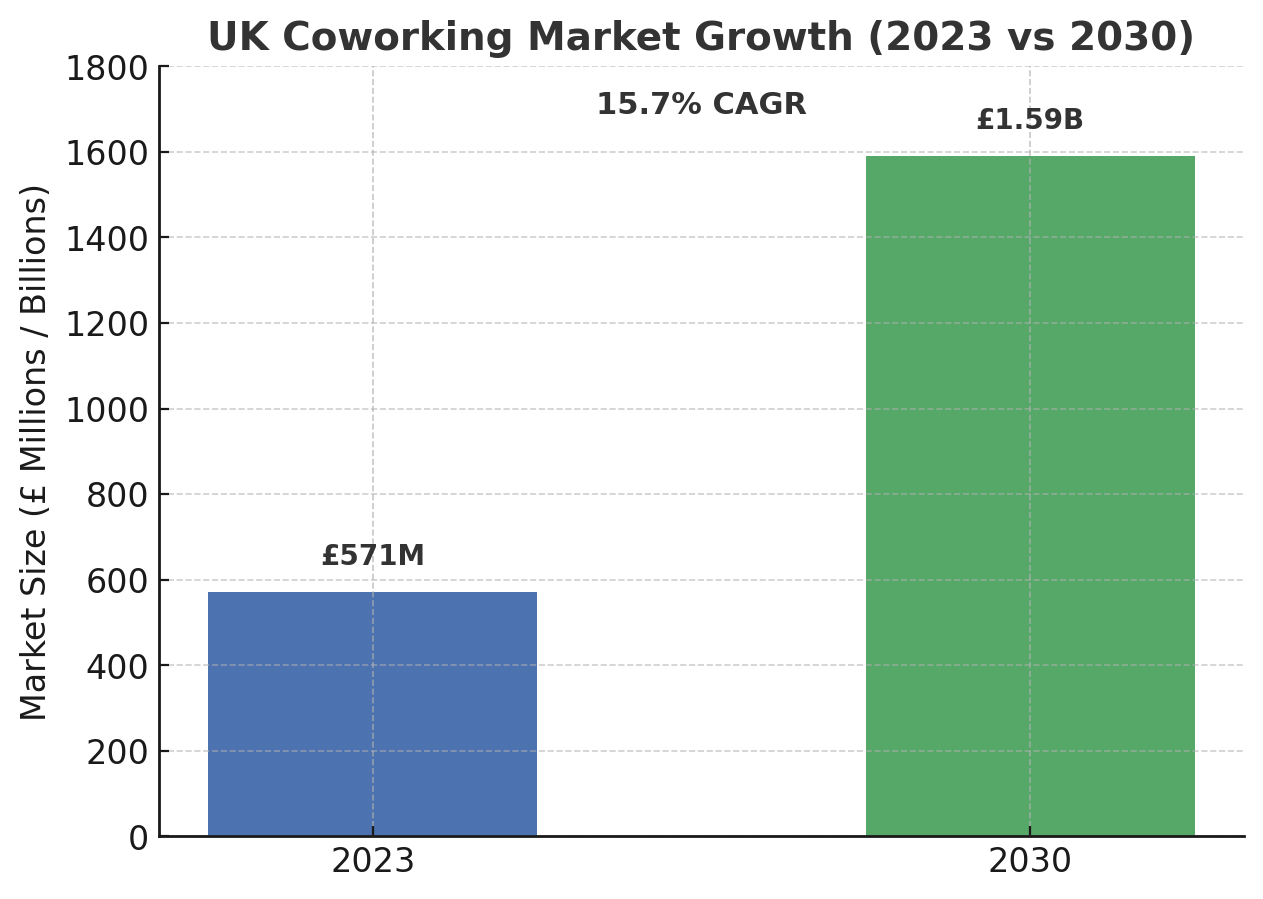

The UK coworking market in 2025 is defined by rapid expansion, maturing demand, and increasingly nuanced regional dynamics. Whether you’re running a space, investing in the sector, or choosing where to work, the data points to several clear opportunities.

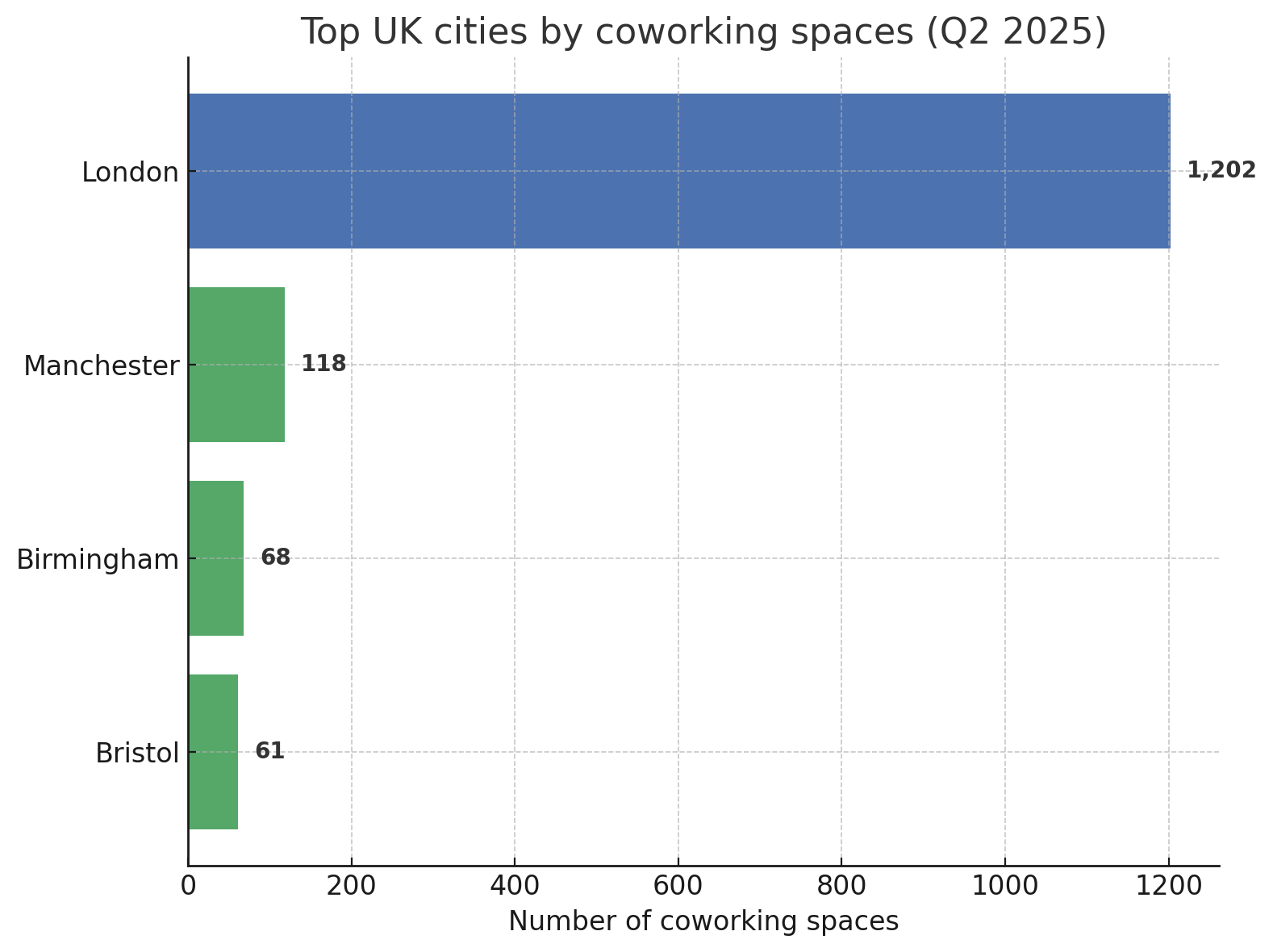

- Think beyond London: while the capital remains a lucrative market, growth in Manchester, Birmingham, Leeds, and Bristol offers strong potential at lower operating costs.

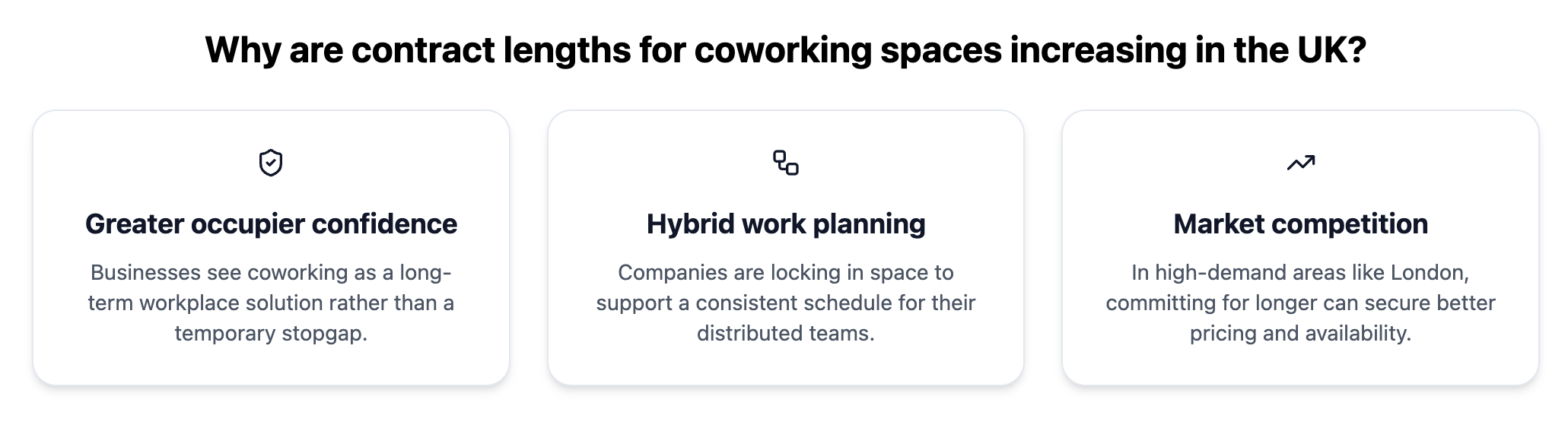

- Leverage longer commitments: the rise in average contract length to 22 months means more predictable revenue streams.

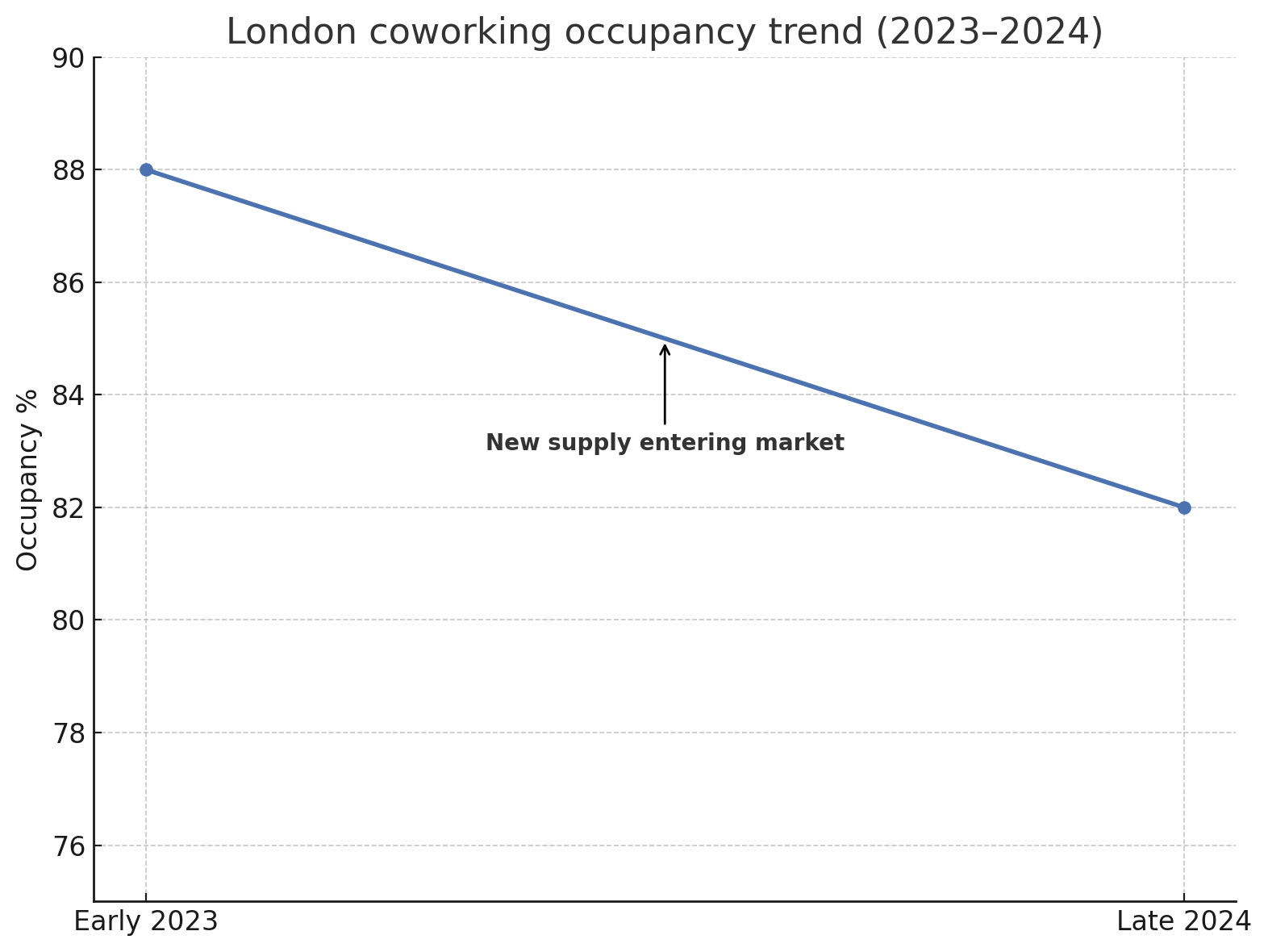

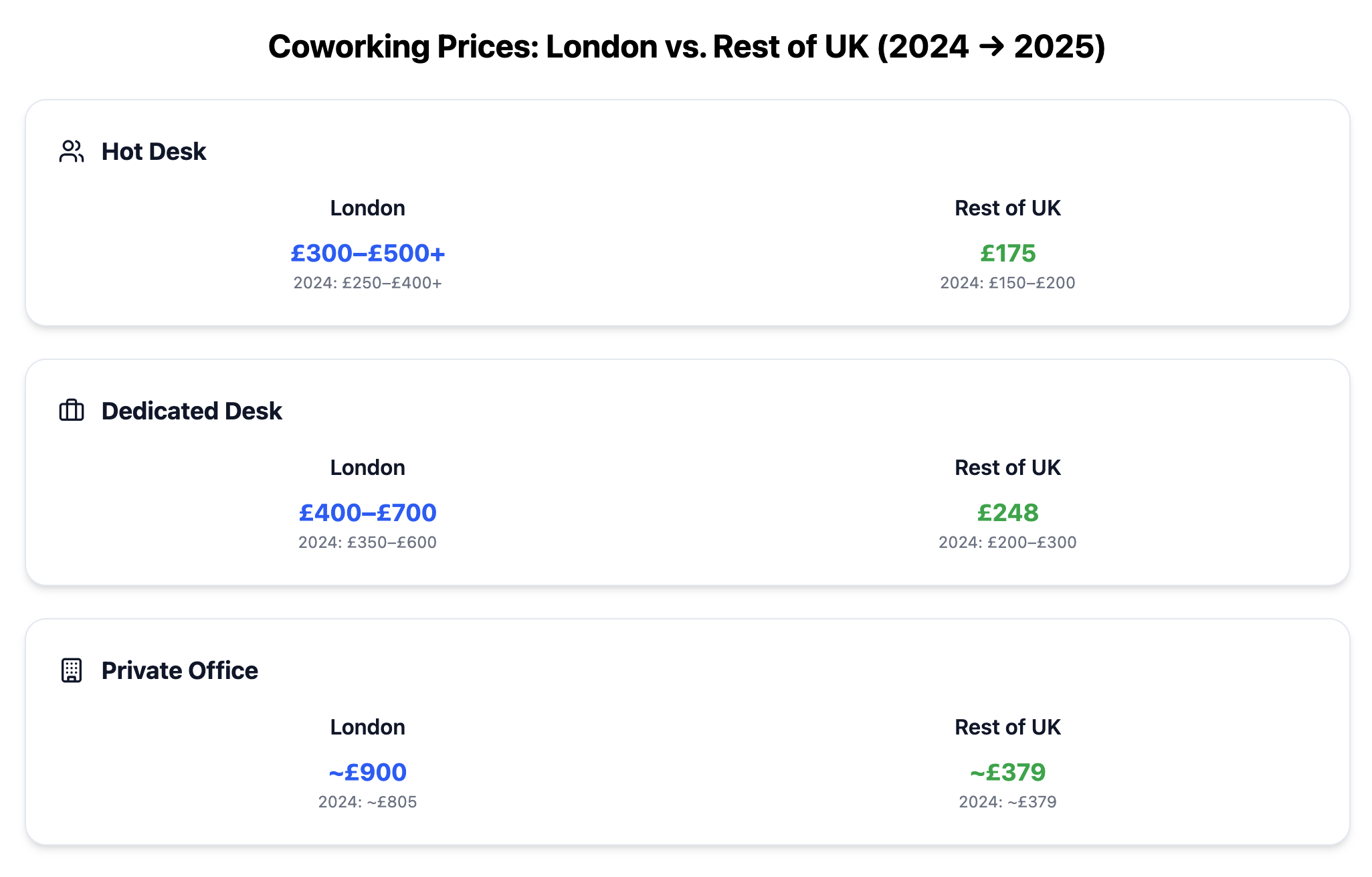

- Prepare for pricing differentiation: London’s premium price supports higher service levels and brand positioning, but regional markets may require competitive pricing and tailored amenities.

- Capitalize on hybrid work trends: flexible memberships and satellite office models are attracting corporate clients, design packages that cater specifically to this demand.

The UK coworking industry is maturing into a stable, diverse market. For operators, the playbook now extends beyond simply filling desks—it’s about targeting the right locations, securing longer commitments, and offering differentiated value.

Are you a UK-based coworking space operator looking for a way to automate your coworking space and improve profitability? Get in touch with Optix.