Emerging trends to watch

- Coliving + coworking hybrids: popular in Southern Europe and tourist-friendly cities, blending accommodation and workspace for remote workers and digital nomads.

- Wellness-integrated workspaces: expect more operators to offer gyms, meditation rooms, and wellness programs as differentiators.

- Industry-specific coworking: niche spaces tailored for sectors like biotech, design, or legal professionals.

- Suburban and secondary city growth: operators targeting less saturated areas with high remote worker populations.

Potential challenges

- Economic headwinds: recessionary trends or interest rate fluctuations could slow expansion plans or pressure pricing.

- Remote work policy shifts: if large corporates revert to primarily office-based work, demand for flex space could soften in some markets.

- Operator sustainability: profitability remains a focus, with overexpansion risks now carefully monitored after lessons learned pre-2020.

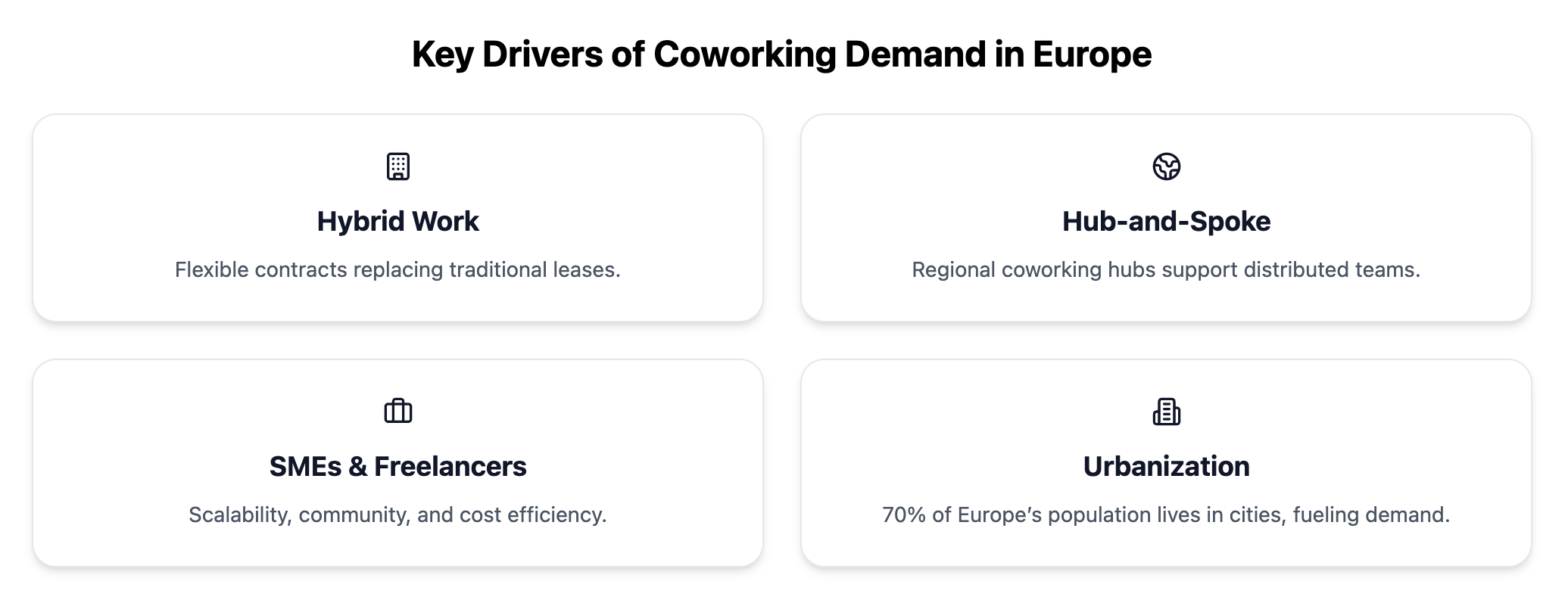

Coworking has become an integral part of corporate real estate strategies across Europe. The period from 2025 to 2030 will likely see the sector deepen its penetration, diversify its formats, and play a key role in shaping the future of work on the continent.

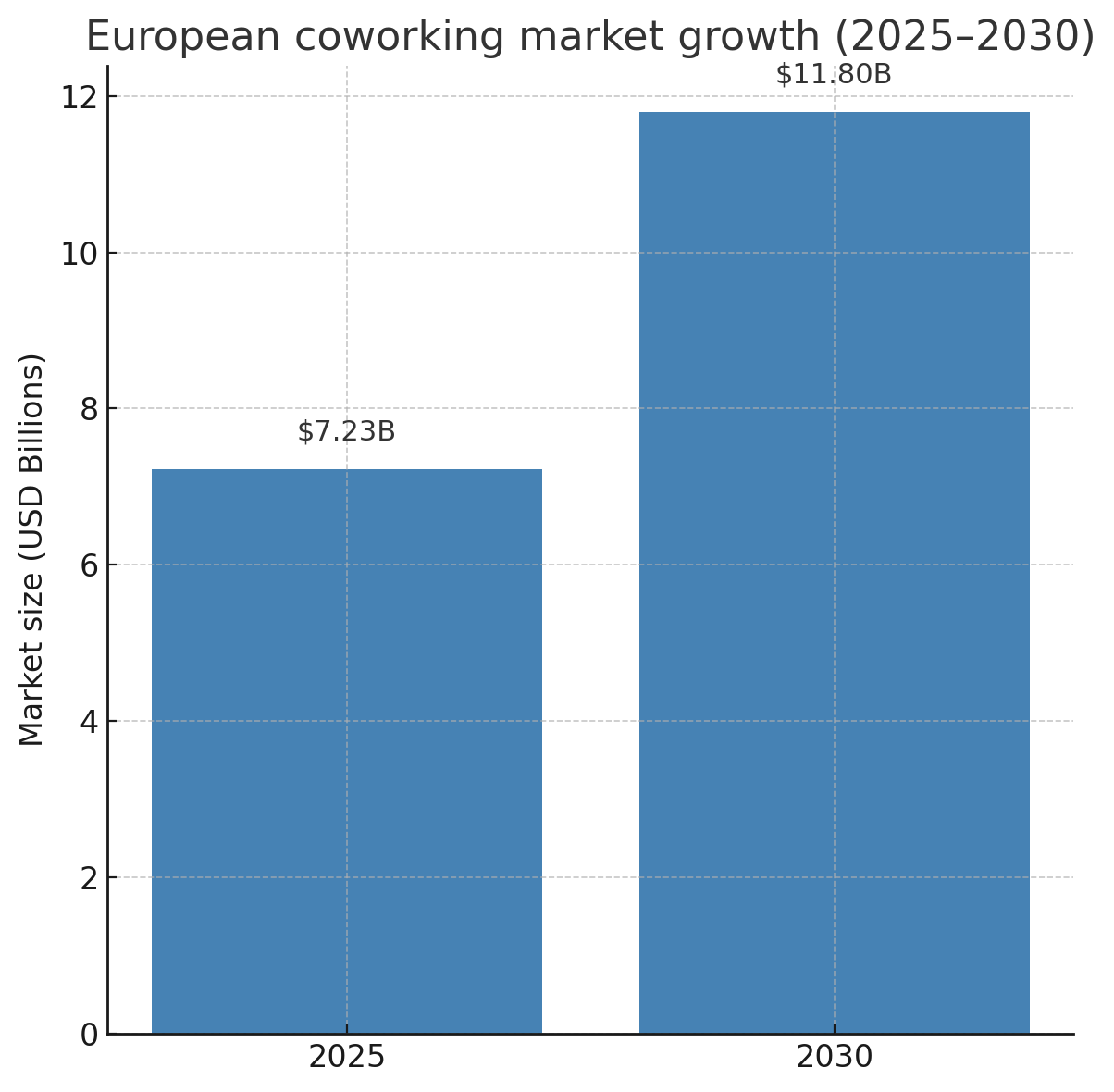

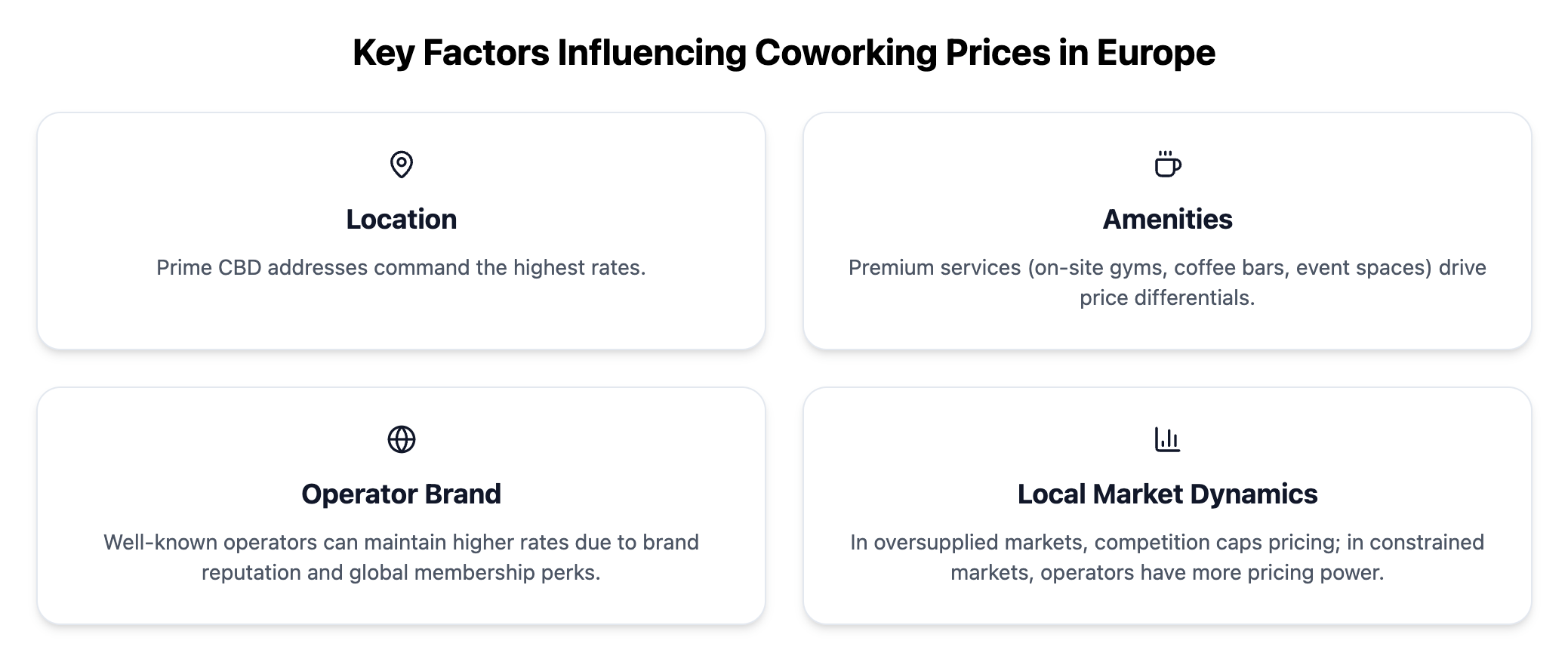

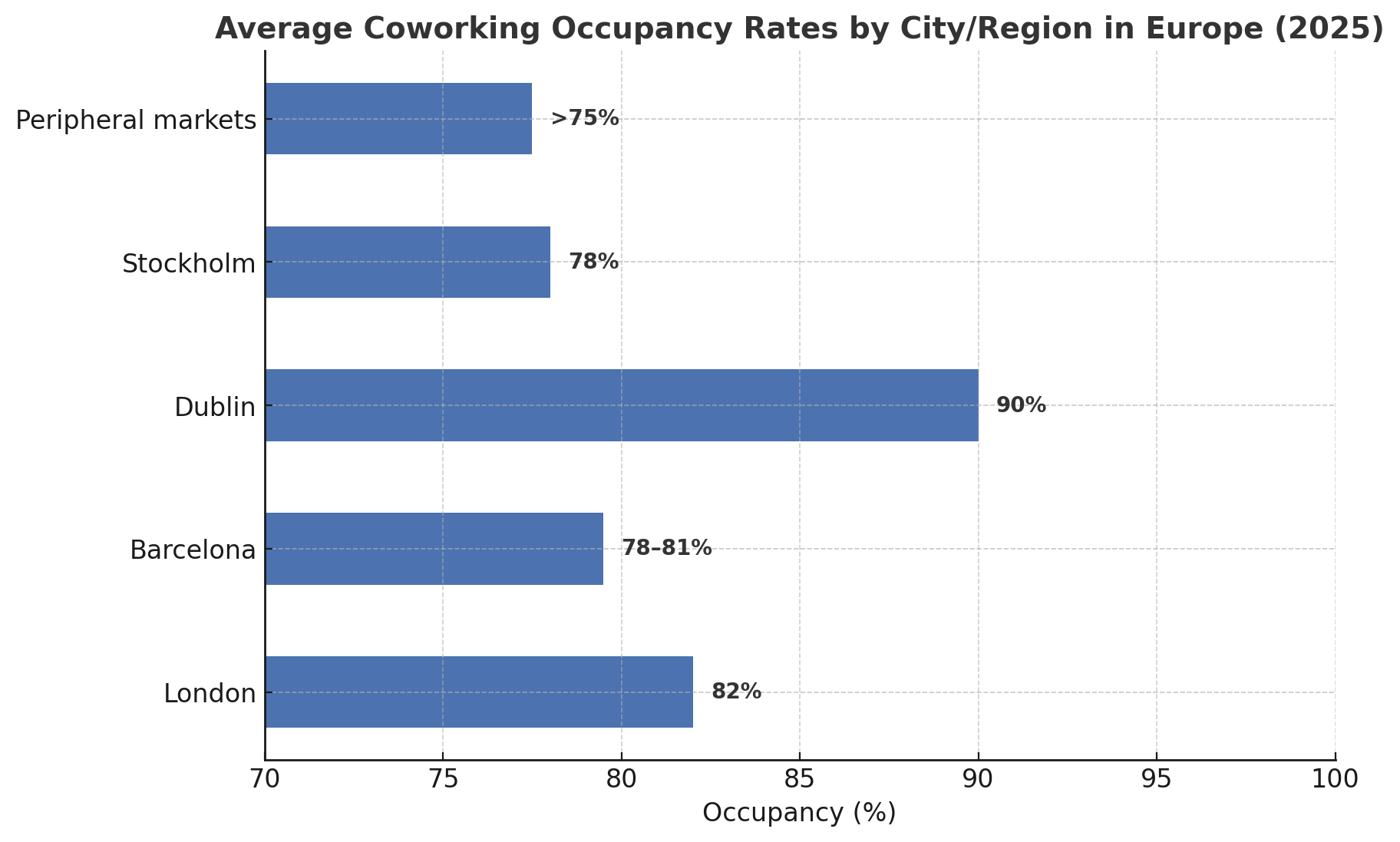

The European coworking industry is growing

The European coworking and flexible office market is no longer a niche but a vital part of the continent’s commercial real estate landscape.

With market value climbing steadily toward USD 11.8 billion by 2030, strong occupancy rates well above traditional offices, and growing adoption across both major cities and regional hubs, the sector is positioned for sustained growth.

As hybrid work models mature, demand from SMEs, freelancers, and corporations alike will continue to drive expansion, with flexible space expected to account for up to 30% of Europe’s office stock in the coming years.